Homeownership Made Easy: The Simple Guide to Budgeting for Your New House

Let’s be honest: the second buyers get the keys to their new place, they feel like everyone is trying to get into their wallet. Between the "must-have" appliances and realizing that a lawnmower is actually an investment, the "new homeowner" phase can be a lot.

In 2026, buyers aren't just spending; they're being smart. Here is the easiest way buyers can teach themselves how to budget so they can actually enjoy your home without the stress.

The "30% Rule": Is Your House Costing Too Much?

There is a very simple limit you should try to stay under. If more than 30% of your monthly paycheck goes toward your housing (mortgage, taxes, and insurance), you are officially "Housing Burdened." Basically, that’s just a fancy way of saying your house is eating too much of your income. When you go over that 30% mark, you start feeling "house poor," meaning you have a beautiful home but no money left over for groceries, gas, or a night out.

How to calculate your percentage (The Easy Way):

1. Open your phone calculator.

2. Add up your Total Monthly House Payment (Mortgage + Insurance + Tax).

3. Divide that number by your Total Monthly Take-Home Pay.

4. Multiply by 100.

Example: If your house payment is $1,800 and your paycheck is $6,000:

$1,800 ÷ $6,000 = 0.30

$0.30 x 100 = 30%.

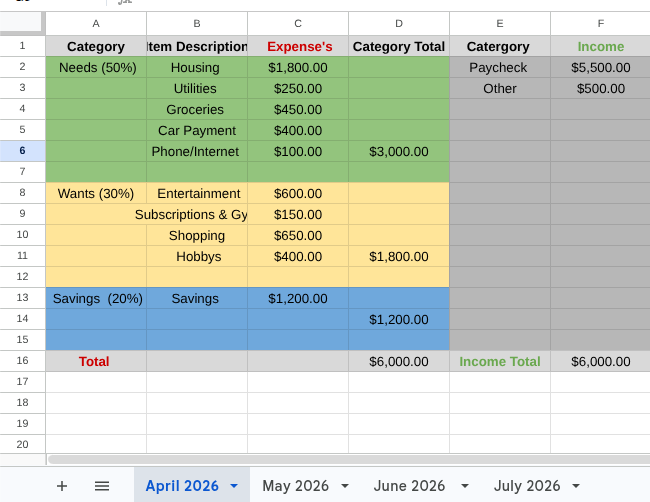

The 50/30/20 Plan: A Simple Balance

To keep your bank account healthy, use the 50/30/20 rule. It’s the most straightforward way to divide your money so every dollar has a job:

50% for Needs: These are the "Must-Pay" bills. This includes your mortgage, utilities (water/electric), and basic groceries.

30% for Wants: This is for your lifestyle. The new rug, dinner with friends, or travel plans.

20% for Savings for Emergencies or Goals: This is your safety net for when the AC breaks, or your fund to save up for something big, like a future renovation.

The Ten-Minute Monthly Spreadsheet

You don’t need to be a math expert to track your money. You just need a simple layout that does the hard work for you. Here is how to set up your sheet to stay organized:

1. The Two-Side Balance

Instead of one long, confusing list, split your screen into two sides. Put your Expenses (Needs, Wants, and Savings) on the left and your Income (paychecks) on the right. This shows you exactly what you have to work with at a glance.

2. Monthly Tabs

At the bottom of your spreadsheet, click the "+" icon to make 12 tabs and name them January through December. This is a game-changer because your electric bill in July will look way different from what it does in April. Having a tab for every month lets you look back and actually plan for those changes.

3. The "Auto-Math" Magic

In Google Sheets or Excel, you don't have to add things up yourself. Just highlight your "Amount" column and click the Σ (Sum) button. The computer adds it all up for you instantly!

The "Observation Month" Strategy

Before you rush out to buy furniture for every single room, give yourself one month to just live in the house with what you have. You’ll quickly realize that the "need" for a $500 rug isn't as high as the "need" for a solid security system or a new set of air filters.

Bottom Line

At Mynor & Associates, we want you to love your home. Budgeting isn't about saying "no" to everything; it’s about having the freedom to say "yes" to the things that actually matter. When you know where every dollar is going, you are in charge of your house—not the other way around.

Beyond the Showroom: Giving Your Home a Soul with Vintage Finds